Las Vegas & Henderson Housing Market Update: 2023 Reflections & 2024 Projections

As we bid farewell to 2023, the real estate market in Southern Nevada concludes on a high note, reflecting a resilient landscape. Home prices rose, marking a noteworthy 5.9% increase in the median sales price, now standing at $449,900 for single-family homes. This upward trajectory is particularly rewarding for those who made their home purchases during the vibrant spring of 2022 when the market reached its high point. Although the market experienced corrections in the 3rd and 4th quarters of 2022, the current median price, while slightly below the peak of $480,000 in April–June 2022, signifies a robust market recovery. Yet, the ever-present concern of affordability lingers over Southern Nevada's housing scene.

Intriguingly, interest rates, which have been under the watchful eye of market participants, started showing signs of a gentle decline in late December. Projections indicate a further decrease in the 2nd or 3rd quarter of 2024, with inflation emerging as the driving force behind these adjustments. The Federal Reserve closely monitors job and wage growth as pivotal indicators, and the early weeks of 2024 have already exceeded expectations in employment growth. This unexpected surge is anticipated to shift the timeline for lower interest rates from the 1st quarter to the 2nd or 3rd quarter of 2024.

While the median sales price captures headlines, our scrutiny extends to other critical metrics shaping housing trends—namely, inventory and sales velocity. To understand the market dynamics of 2023, let's delve into the data and results.

What were the trends in 2023? Median Sales Price: Flat 3rd & 4th Qrt | Median Home Size: Flat | # of Homes Sold: ↓ | Days on Market: ↓ | Inventory: Up & Down by quarter but significantly down from year-end 2022 | Sales Volume: ↓ 17% from 2022 and ↓ almost 50% from 2021, which was our 5-year high.

CORE FACTORS AFFECTING THE MARKET

Mortgage Rates

Navigating the currents of the real estate market in 2023, one stubborn factor persists—mortgage rates. Throughout most of the year, these rates held steadfastly above 7%, casting a shadow on buyer demand and discouraging sellers from listing their homes. A brief respite in March saw rates dipping into the low 6% range, sparking a surge in mortgage applications, and providing a glimmer of optimism. Notably, mortgage applications serve as a leading indicator, offering insights into the resale housing market's direction 60 days later.

Amidst this backdrop, a burning question echoes across the minds of buyers, sellers, business owners, and investors alike—what lies ahead for 2024? This pivotal query directly impacts companies' growth prospects and buyer's capacity to enter the housing market. Anticipating the trends, the following graphs summarize the predictions of leading housing economists for mortgage rates in the upcoming year. It offers a glimpse into the financial landscape that will shape the real estate journey this year.

Note: Conventional rates have been running 0.5% higher than FHA and VA

Early this month, the Mortgage Reports published an article providing this graph indicating relative agreement from the five Housing Authorities that mortgage rates in 1st quarter 2024 will remain close to the 7% range for conventional mortgages. FHA and VA have been trending 0.5% below conventional mortgages.

Source: https://themortgagereports.com/32667/mortgage-rates-forecast-fha-va-usda-conventional

Although not directly tied, mortgage rates have historically run in concert with the 10-year Treasury yield. The following graph shows the spread between the 30-year mortgage rate and the 10-year Treasury yield.

Graph Source: https://money.usnews.com/loans/mortgages/mortgage-rate-forecast#:~:text=MBA%3A%20Rates%20Will%20Decline%20to,the%20first%20quarter%20of%202025.

As mortgage rates maintain their grip between 6% to 7%, a pivotal question emerges—how will this range impact the median home price?

The top housing authorities have recently revealed their 2024 predictions, inviting a fascinating comparison to our June housing market report. Our analysis reveals that the predictions marked in green are close to what we expect and the ones in red show big differences, either much higher or much lower than expected. Examining their prior national-level forecasts for the 3-year span from 2023 to 2026, we find Zillow and CoreLogic leading the accuracy race with a 3.1-3.4% increase. In contrast, Southern Nevada outshone expectations at 5.9%, nearly doubling even the most optimistic projections. A consensus among housing authorities suggests a 2024 appreciation in the 3% or less range.

Here was their previous prediction of home prices at the national level for the 3-year period from 2023 to 2026:

- Zillow predicts home values will increase in 2023 5% | 2024 3.4% | 2025 3.3% | 2026 3.2%

- Nation Association of Realtors (July 2023) expects a drop in 2023 by 9% over 2022 and an increase in 2024 by 15.5%.

- We believe this prediction will be adjusted based upon the current pricing averages both for Nevada and on the national level.

- Goldman Sachs: 2023 2% | 2024 3.5% | 2025 4% | 2026 4%

- Case-Shiller: 2023 3% | 2024 1.7% | 2025 2.4% | 2026 3.8%

- Corelogic: 2023 1% | 2024 3.4% | 2025 4% | 2026 4%

Source: https://www.statista.com/statistics/226144/us-existing-home-sales/

Zillow and Corelogic were the closest at the 3.1- 3.4% increase whereas here in So. Nevada, we were at 5.9; so nearly double the most aggressive predictions. It is a consensus with all the housing authority’s economists that 2024’s appreciation is expected to be in the 3% or less range.

Supply and Demand

The dynamics of supply and demand wield a direct influence on home prices and purchase terms. Our focus now extends to Nevada's population growth, rooted in migration predictions for 2024. Nation Van Lines anticipates a net migration gain of 1,772 individuals. Diving deeper into the demographics, the US Census Report from April 2023 reveals that Gen Z and Millennials lead the charge, with an expected 39% and 28% considering a move, respectively, while baby boomers trail at 18%. Adding to the narrative, Moving.com's article outlines the top 9 reasons people are inclined to relocate:

- To have more affordable housing or lower cost of living

- To live in a safer area

- Moving for a new job

- To be closer to family and friends

- To live in an area more aligned with beliefs

- Better schools

- Lower taxes

- Effects of climate change

- Job requirements to be back in the office

Affordability

The gap between the median income in Southern Nevada and the amount of income required to qualify for the median home price is widening. Using the predictions above, we have forecasted the required income to qualify for a home purchase over the next 3 years.

Note: Assumes Conventional loan, 5% down payment, 33% of household income applied toward house payment (PITI).

We have concerns that home price prediction in the 3% range may be unaccounted, especially when rates drop and the demand of buyers flood the market.

Only 33.1% of Southern Nevadans have a median household income sufficient to afford the median sales priced home. According to a graph provided by Applied Analysis, this figure is projected to move to about 40% in the next five years.

RENTAL MARKET

The median rent for a single-family home has followed the sales market remaining relative flat since 1st quarter. The median lease rate is $2,100 for +/- 1,841 sf home. The median price-per-square foot is $1.16 with new homes or updated homes still obtaining a premium. The days-on-market (time it takes to lease a home) has increased quarter-over-quarter at 27 days.

As a reminder from our last report, most landlord qualifications require 3x the rent of monthly income. From the household income graph mentioned earlier, this means less than 47% of households in Southern Nevada can afford the median rent.

HOUSING SNAPSHOT

Let’s review a snapshot of what happened in the 4th quarter of 2023:

OUR TAKEAWAY

What is expected to occur in 2024?

- Sales Prices: We expect home prices to be around 3% appreciation, year-over-year, with a jump when rates drop closer to 6%.

- Interest Rates: Hold in the 6.75% to 7% for 1st quarter, decreasing slightly in 2nd and 3rd and then around 5.75% to 6% in 4th quarter.

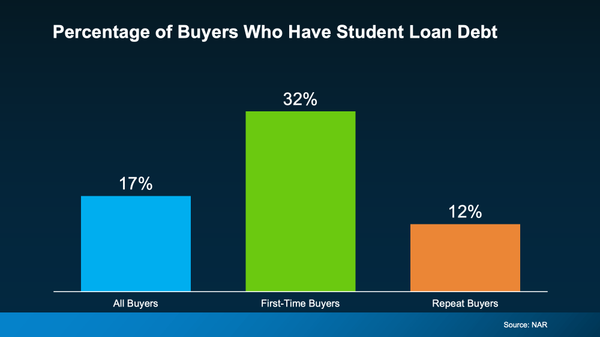

- Foreclosures: Very low rates. With credit card debt increasing and student loan payment deferral at an end, we expect that foreclosures will ever so slightly increase.

- Inventory: We expect the number of homes on the market to remain low; however, the days-on-market lower from March thru June.

- Rental Rates to Flatten: Maintain the median price of $1.15 to $1.20.

Buyer Opportunities

- Moderate Selection: Inventory to remain low and with a predicted jump up in buyer activity in the spring. When rates decline, buyers could be facing a multi-offer competition, but only a couple per home (nothing like the 2021 frenzy).

- Be Prepared: We have many buyers who are waiting for rates to be closer to 6% before making a home purchase, as the debt-to-income ratios do not work for qualifying at today’s rate. We have been telling our future buyers to GET PREPARED! Do all that you can now to be ahead of the wave when rates drop. There are a few simple things future buyers can do to provide them even more competitive rates and the best options when for mortgage rates. We’ve held a lot of buyer consultations this last quarter which has allowed our clients to do the small things. This includes moving their credit score (even those with excellent credit can move up), because the stronger your credit score, the lower your interest rate.

- Less Out-of-Pocket Expenses

- No more over-appraisal value offers unless a home has the sizzle and pop.

- Sellers are willing to contribute to buyer’s closing costs.

- Sellers are willing to accept offers with programs with down payment assistance.

- More Favorable Terms

- Repair requests will be more evenly considered now.

- Buyers can really think about the homes they tour and decide on the best one for them, no pressure to make a same-day decision.

- No competing with multiple offers.

- Longer close of escrow (COE) periods. If you are in a lease and need time to coordinate the end of your lease term closer to the COE, we have successfully negotiated longer dates so it reduces costs and gives you more time, therefore relieving stress.

- Affordability: Never buy more home than you can afford. We never want our clients to be house poor. Financial Advisors and Mortgage lenders recommend the range of 25% to 35% of your gross monthly income to be put towards your home mortgage payment (Principle, Interest, Tax, Insurance = PITI). For those who have the income to qualify, and it fits their family’s budget, buying ahead of the wave of buyers may provide them the best deal. Many of our lender partners offer their clients a one-time rate adjustment within 3 to 5 years. If your budget allows, this can give you the advantage at today’s home price and then a reset if and when mortgage rates drop. Never speculate on rates dropping; only purchase a home that fits your budget.

- New Home Option: New homes continue to provide the best interest rates as builders are still offering incentives. We expect this will slow down and the incentives will drop off first, and then the mortgage rate discounts. The mortgage rate discounts being offered today range between 5-6%, with a 5-10% down payment. The most highly desired new home communities will be offering less incentives. We have a weekly update of the incentives being offered by each builder.

- Renting Will Still Be Expensive

- If you rent a home for $2,150 for 3 years, you just paid your landlord $77,400 with no equity, no gain.

If you really want to own a home in the next couple of years, reduce the size of home you are currently renting and put away the difference in rent. It will also prepare you for the size of home you can afford to purchase. We foresee the rents will run lower than the purchasing options on a monthly basis, before appreciation and accounting for principal reduction

Seller Opportunities

Price-to-market value: even in the spring, the market moved slightly towards a seller’s market. Sellers who overpriced their homes sat on the market. When a home sits on the market, you lose buyer appeal for the home and the eventual achieved price in most cases will be lower than if you priced the home to market. No need to price under market. If you price to market, you will have several offers to select from and will be able to identify the best buyer on price, terms, and qualifications. We expect buyer demand to decrease in 3rd quarter based upon mortgage applications rates today.

Our advice:

- Review the market comparable and be realistic with your home’s current value.

- Marketing your home will be extremely important. Having a high-quality online presence is crucial.

- Have patience: it will take longer to sell. 68% of homes sold in 30 days; we expect to see that number drop in 3rd and 4th quarter. In the Springtime, you can expect 30 to 45 days; fall and winter closer to 60. If you price over market, it will take quite some time. Your home will get a lot of tours before a buyer offer is received. Buyers want to see many options before deciding on a home.

- Buyer terms: expect home buyers to ask for closing cost credits and repairs.

- We are seeing a lot more seller occupied homes on the market, we can negotiate terms that allow the Seller to remain in the home for up to 60 days (sometimes longer, depending on the buyer’s mortgage) which allows our sellers to make stronger offers on their home purchases. It also takes the stress out of the buyer’s contingency, especially loan contingency. Lenders are tightening their standards and requiring a lot more documentation. Many lenders have reduced staff, so they are not hitting their time frames. By negotiating a post occupancy option for our sellers, we eliminate this stress from the sale.

Questions or comments? Contact Us:

Graham Team Real Estate Advisors

702-930-9551

team@grahamteamnv.com

Categories

Recent Posts